The information in this article is up to date through tax year 2020 (taxes filed 2021).

The IRS recently released a draft of Form 1040, U.S. Individual Income Tax Return. Here is a look at some of the most significant changes proposed for tax year 2020 (returns filed in 2021). Please note: The information below is subject to change. The draft of Form 1040 should not be used to file your clients’ taxes.

Stimulus checks and the Recovery Rebate Credit

According to the draft, a new Line 30 has been added on page two of Form 1040 for the “Recovery Rebate Credit.” This is where taxpayers who did not get the payments or should have received larger payments (due to birth of child or changes in income) will enter the additional amount due. This amount will be treated as a refundable credit. The reconciliation of stimulus payments will be done on a worksheet contained in the Form 1040 Instruction, which has not yet been released.

CARES Act relief

The “Amount You Owe” section of the new 1040 now says, “Schedule H and Schedule SE filers, line 37 may not represent all of the taxes you owe for 2020.” This is because, under the CARES Act, employers can defer deposits and payments of the employer’s share of Social Security tax that would otherwise be required to be made between March 27, 2020 and December 31, 2020. This deferred amount will be reported in the Payments section of Form 1040, Schedule 3, Line 12e as a “Deferral for certain Schedule H or SE filers.”

For self-employed taxpayers, a third page is being added to the Schedule SE where the deferred portion of the self-employment tax will be calculated. Schedule H will also be redesigned to address the deferred portion of the social security tax deposits made by taxpayers who have household employees.

The new refundable credit for qualified sick and family leave will be entered on Schedule 3, Line 12b. The credit amount will be calculated on Form 7202, which the IRS has not released yet in draft form.

Above-the-line charitable contributions

For tax year 2020 only, charitable cash contributions up to $300 will be treated as above-the-line deductions (reported on Schedule A). The new Line 10b is for charitable contributions for taxpayers taking the standard deduction.

Reporting income tax withholding

Instead of a single line for federal income tax withholding, the new Form 1040 has three separate lines for withholdings: Line 25a is for Form W-2, Line 25b is for Form 1099, Line 25c is for other forms (see instructions). Line 25d is the total tax withholdings. This should make withholding reconciliation much easier for tax preparers to recognize.

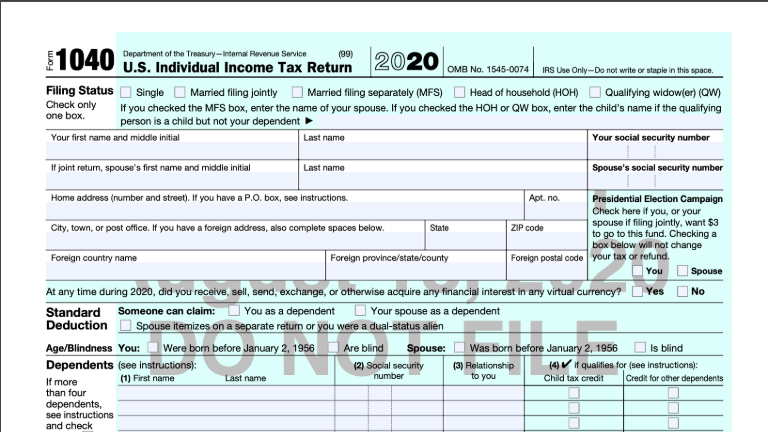

Reporting cryptocurrency

The question about virtual currency first appeared in 2019 as a checkbox at the top of Schedule 1, Additional Income and Adjustments to Income. For tax year 2020, the question “At any time during 2020, did you receive, sell, exchange, or otherwise acquire any financial interest in any virtual currency?” has been moved just below the taxpayer’s name and address on the main Form 1040.

The IRS has taken the position that virtual currency is considered investment property, and any transaction involving the sale or exchange of virtual currency must be accounted for on the tax return just as a taxpayer would account for the sale of any other investment. This will most likely involve a reportable transaction on Form 8949.